This is an update of my A Look at Covered Calls - The Naked Truth project. A hypothetical portfolio of systematic covered call writing (AKA synthetic naked put writing) with a non-margin account.

***

Although I haven't posted in a while and didn't update May results, I have been recording the hypothetical trades in real time. It is now six cycles with a bull phase and bear phase included. This has been fortuitous as it has been handy to show largely what I have been wanting to demonstrate about covered calls.

Going back to my original motivation for this simulation, it was to expose the nonsense of the ubiquitous advertising line that one could make 4-8% income every month from this strategy.

This simulation is not the perfect example of how everyone would trade covered calls, but by now shows the problems inherent in the strategy as a systematic income generation machine.

I should point out that I am not against covered calls in the slightest. I use them (or the pure version of the strategy, the short put) frequently when I want that particular risk profile. I have some long term holdings that I sometimes write calls over when I think it is appropriate, but never systematically every cycle.

The fact of covered calls is that they are optimally profitable when the stock moves sideways. They under perform their underlying market in strong up-trends and outperform their underlying market (though may still make losses) in down-trends. Over the long term they reduce volatility, but depending on the greater trend there is no guarantee that they will be outperform the underlying.

I do not believe picking and choosing tickers (systematically) works any better than picking and choosing underlying stocks in a trading system.

Several 'educators' try to rework the numbers by altering the moneyness of the options, most frequently by writing deep in the money. This increases probability of profit, which feels good to the investor who enjoys large numbers of wins, but dramatically reduces the maximum profit. It also dramatically increases the size of the (abeit fewer) losses as a proportion to the typical win.

It changes the nature of the equity curve, but not the ultimate expectancy. It's a bit like a martingale system. it feels like you have found the holy grail for a while, until you get run over by the proverbial steam roller.

OK lets look at the graphs of the individual stocks I am using along with the total list of trades with the last two month's trades beneath the screen split.

As at close of trading June 15 2012:

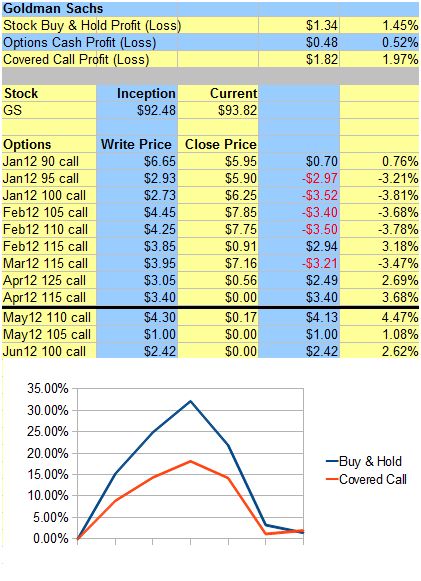

Goldman Sachs

After six months trading, an impressive run up, an equally impressive swoon, we are essentially back where we started with both the underlying and the covered call strategy. All we have managed to achieve is to reduce volatility.

But this is a classic illustration of how CCs under perform the underlying in up-trends and outperforms the underlying in down and sideways trends.

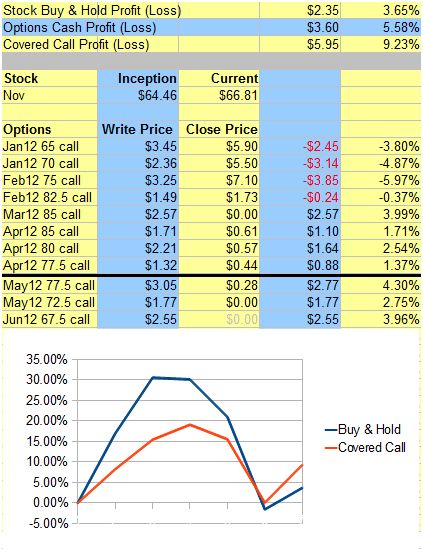

National Oilwell Varco

NOV has not been that dissimilar to GS, excepting that the CC strategy has managed to augment our equity by 5.5% over the six months. That's not a bad result for a buy an hold investor, but a far cry from the 4-8% per month as claimed by the seminar clowns.

Freeport McMoran

FCX represents the most significant out-performance of the three stocks selected at ~7.5%, but really has only trimmed the nearly 9% loss on the underlying to 1%. If you are invested in FCX on a buy and hold basis, that is a significant achievement... and that 7.5% is cash you can use for a festive dinner with friends and family, or reinvest if you prefer, but still nothing like the "buy my $3,000 covered call course" promoters claim.

Yes some of the returns in individual months were 4-8%, but mostly at the cost of even greater returns from the underlying. In other words investors trying to pick uptrends to write covered calls would have been better off just buying the underlying.

However, there is still good times to write calls in up-trends. One can dust off their crystal ball and write calls a bit out of the money at points where the underlying is overbought and likely to retrace or consolidate in the time frame selected (time til expiry).

As shown, they also partially hedge in downtrends. But the best use of covered calls is if you can see into the future and pick when your stock is going to go sideways.

Overall, a useful strategy for investors, but sub-optimal for shorter term traders.